Investment Insight | Reporting season

New Zealand company earnings

The shortest, sharpest recession in living memory gives way to a new early-cycle phase. We expect improving economic data and earnings in the final quarter of 2020 to continue to push shares up. However, risks remain meaningful, suggesting we will have to contend with lingering volatility.

Risk, both to the upside and the downside, is evidenced in the earnings announcements of New Zealand listed companies over the past few weeks. Colloquially known as ‘reporting season’ it is a time when companies update investors on their financial results and outlook. The pandemic and its economic aftermath have given rise to ‘haves’ and ‘have nots’ in our economy. Below we describe some of the headlines from the August reporting season.

The good

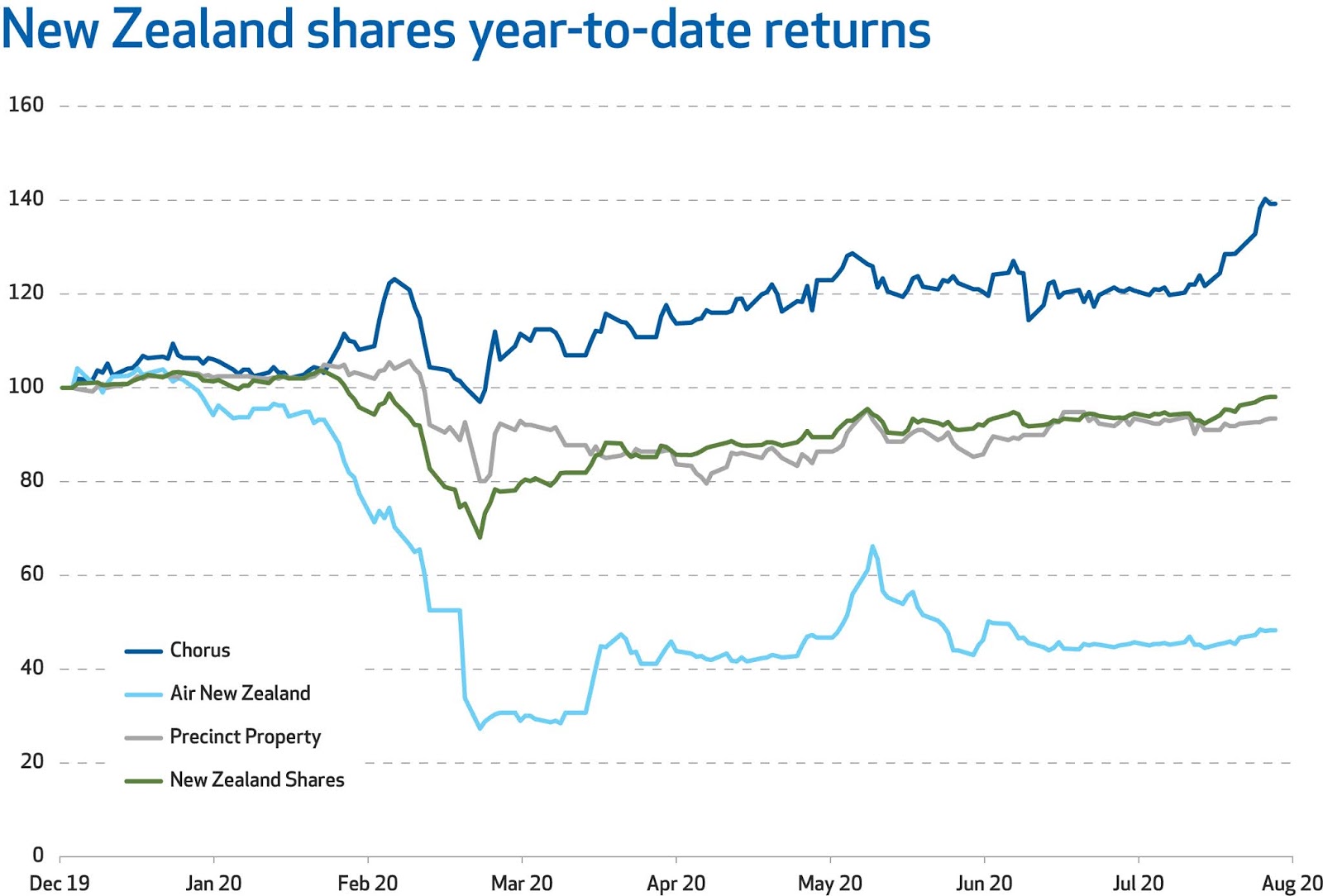

Chorus is New Zealand’s largest telecommunications infrastructure company and is building the country’s fixed Ultra-Fast Broadband (UFB) telecommunications network.

This week, the Chorus share price recorded new highs. This is a far cry from the indebted spinout of Telecom New Zealand it started life as in 2011. Chorus has benefited from a more digitised world and given the success in the uptake of fibre in New Zealand, investors will soon start reaping the benefits.

The key piece of news in Chorus’s result was the company’s confirmation of its new cashflow-based dividend policy that will take effect from 2022. This will ultimately lead to a significant step change from the forecast 2021 dividend of 25 cent per share. The math suggests that from 2024 Chorus should be able to pay dividends of 50 to 60 cents per share. This is an 11%-plus yield on today’s share price.

The not so good

This is in stark contrast to the Air New Zealand result. While most could guess the earnings announcement was not going to be positive, Air New Zealand’s results really highlight the severe operational and financial impact of COVID-19 on the global airline industry.

Air New Zealand reported its first negative earnings in 18 years with a loss of $87 million (before other significant items). This is a drastic decrease compared to the $387 million profit it reported last year, given COVID-19 only impacted the last 4 months of their financial year.

Of immediate concern to investors is Air New Zealand’s liquidity position and the level of cash it continues to burn each month. Before the crisis began, Air New Zealand had over $1 billion in available cash on its balance sheet. This number has now reduced to $200 million. According to the outlook provided by the company in its announcement on 27 August, Air New Zealand will continue to burn cash at a rate of approximately $75 million per month.

Air New Zealand has yet to draw on the $900 million debt package provided by the government, so we estimate it has 12 months to find a longer-term solution to its capital structure problems. While there is no news of any immediate equity raise, the company did comment that they are working constructively with the NZ Government who are the majority shareholder.

The interesting

Precinct Properties owns prime, central business district office properties in Auckland and Wellington, including recently completed Commercial Bay in Auckland. There had been concern earlier this year that the work from home culture could damage demand for office space, putting pressure on Precinct’s earnings.

At its result in mid-August, Precinct commented that while it has seen the agile workforce increase from around 10% to 20% post COVID-19, the importance of the workplace for collaboration, creativity and culture means it doesn’t foresee a significant decrease in demand for office space.

Perhaps most surprising was Commercial Bay’s retail offering which opened strongly with pedestrian count exceeding expectations. A huge achievement, given it opened not long after New Zealand emerged from level 4 lockdown and dismissing the theory that the new offering was reliant on cruise ships into Auckland’s harbour.

Precincts’ share price has been volatile since March. It initially suffered given the immediate perceived effects COVID-19 could have on its tenants’ abilities to pay rent. However, the quality of the buildings within its portfolio and overreaction of the market to the work at home culture shift has presented a buying opportunity for a long-term high quality and liquid exposure to commercial property.

Investment philosophy

As we discussed in 10 July 2020 | NZ Funds Investment Philosophy, our active management approach enables us to better meet the objectives of each Portfolio we invest and take advantage of investment opportunities as they arise. In times of volatility, active management guides clients’ portfolios through cycles, whether they be economic or company specific.

This divergence in earnings outlook from companies emphasises the need for share-specific research to help identify high-quality companies that can weather the storms. Chorus, Air New Zealand, and Precinct highlight the different reactions of companies and their earnings to the pandemic gripping the globe and inform us as to how we should position clients’ portfolios for the long-term.

Risk, both to the upside and the downside, is evidenced in the earnings announcements of New Zealand listed companies over the past few weeks. Colloquially known as ‘reporting season’ it is a time when companies update investors on their financial results and outlook. The pandemic and its economic aftermath have given rise to ‘haves’ and ‘have nots’ in our economy. Below we describe some of the headlines from the August reporting season.

The good

Chorus is New Zealand’s largest telecommunications infrastructure company and is building the country’s fixed Ultra-Fast Broadband (UFB) telecommunications network.

This week, the Chorus share price recorded new highs. This is a far cry from the indebted spinout of Telecom New Zealand it started life as in 2011. Chorus has benefited from a more digitised world and given the success in the uptake of fibre in New Zealand, investors will soon start reaping the benefits.

The key piece of news in Chorus’s result was the company’s confirmation of its new cashflow-based dividend policy that will take effect from 2022. This will ultimately lead to a significant step change from the forecast 2021 dividend of 25 cent per share. The math suggests that from 2024 Chorus should be able to pay dividends of 50 to 60 cents per share. This is an 11%-plus yield on today’s share price.

The not so good

This is in stark contrast to the Air New Zealand result. While most could guess the earnings announcement was not going to be positive, Air New Zealand’s results really highlight the severe operational and financial impact of COVID-19 on the global airline industry.

Air New Zealand reported its first negative earnings in 18 years with a loss of $87 million (before other significant items). This is a drastic decrease compared to the $387 million profit it reported last year, given COVID-19 only impacted the last 4 months of their financial year.

Of immediate concern to investors is Air New Zealand’s liquidity position and the level of cash it continues to burn each month. Before the crisis began, Air New Zealand had over $1 billion in available cash on its balance sheet. This number has now reduced to $200 million. According to the outlook provided by the company in its announcement on 27 August, Air New Zealand will continue to burn cash at a rate of approximately $75 million per month.

Air New Zealand has yet to draw on the $900 million debt package provided by the government, so we estimate it has 12 months to find a longer-term solution to its capital structure problems. While there is no news of any immediate equity raise, the company did comment that they are working constructively with the NZ Government who are the majority shareholder.

The interesting

Precinct Properties owns prime, central business district office properties in Auckland and Wellington, including recently completed Commercial Bay in Auckland. There had been concern earlier this year that the work from home culture could damage demand for office space, putting pressure on Precinct’s earnings.

At its result in mid-August, Precinct commented that while it has seen the agile workforce increase from around 10% to 20% post COVID-19, the importance of the workplace for collaboration, creativity and culture means it doesn’t foresee a significant decrease in demand for office space.

Perhaps most surprising was Commercial Bay’s retail offering which opened strongly with pedestrian count exceeding expectations. A huge achievement, given it opened not long after New Zealand emerged from level 4 lockdown and dismissing the theory that the new offering was reliant on cruise ships into Auckland’s harbour.

Precincts’ share price has been volatile since March. It initially suffered given the immediate perceived effects COVID-19 could have on its tenants’ abilities to pay rent. However, the quality of the buildings within its portfolio and overreaction of the market to the work at home culture shift has presented a buying opportunity for a long-term high quality and liquid exposure to commercial property.

Investment philosophy

As we discussed in 10 July 2020 | NZ Funds Investment Philosophy, our active management approach enables us to better meet the objectives of each Portfolio we invest and take advantage of investment opportunities as they arise. In times of volatility, active management guides clients’ portfolios through cycles, whether they be economic or company specific.

This divergence in earnings outlook from companies emphasises the need for share-specific research to help identify high-quality companies that can weather the storms. Chorus, Air New Zealand, and Precinct highlight the different reactions of companies and their earnings to the pandemic gripping the globe and inform us as to how we should position clients’ portfolios for the long-term.

Source: Bloomberg.

For more information please contact NZ Funds.

This document has been provided for information purposes only. The content of this document is not intended as a substitute for specific professional advice on investments, financial planning or any other matter.

While the information provided in this document is stated accurately to the best of our knowledge and belief, New Zealand Funds Management Limited, its directors, employees and related parties accept no liability or responsibility for any loss, damage, claim or expense suffered or incurred by any party as a result of reliance on the information provided and opinions expressed except as required by law.

For more information please contact NZ Funds.

This document has been provided for information purposes only. The content of this document is not intended as a substitute for specific professional advice on investments, financial planning or any other matter.

While the information provided in this document is stated accurately to the best of our knowledge and belief, New Zealand Funds Management Limited, its directors, employees and related parties accept no liability or responsibility for any loss, damage, claim or expense suffered or incurred by any party as a result of reliance on the information provided and opinions expressed except as required by law.

***

***

James Grigor is Chief Investment Officer for New Zealand Funds Management Limited (NZ Funds) and a member of the NZ Funds KiwiSaver Scheme. James' comments are of a general nature, and he is not responsible for any loss that any reader may suffer from following it.

***